基于ABC的业绩评价体系构建

无需注册登录,支付后按照提示操作即可获取该资料.

基于ABC的业绩评价体系构建(14700字)

摘 要:企业是以经济目标而存在的组织实体,为了衡量其既定目标的实现程度,是离不开一系列评价活动的。随着竞争环境的不断变化迫使企业重新审视经营目标、发展战略和评价体系,新的发展战略与竞争现实,要求我们必须以新观念、新思维、新视角来建立一套能够适应新经济环境和制造方式的业绩评价体系。本文通过分析传统的企业业绩评价体系在新竞争环境下的缺陷,引入作业成本法,构建了以作业成本为基础的业绩综合评价体系,将以财务指标为主的传统业绩评价体系扩充为一个更完善、更有效的综合评价体系。本论文的研究目的是为企业引入一套较为完善的业绩评价工具,更好的帮助企业提高管理水平,改善经营业绩,增强企业的核心竞争力。

关键词:作业成本法;作业成本管理;业绩评价

Study on the Construction of Performance Assessment System Based on the Methodology of Activity-Based Costing

Abstract:Enterprise is an entity for the sake of economic. In order to measure the degree of its organizational goal, it can’t be existed without a series of evaluated activities. Been forced by the constant change of business environment, enterprises must re-examine the business target, the target developmental strategy and the system of evaluation. The new developmental strategy and completive reality require us build a system of performance evaluation, based on new concept, thinking and perspective, in order to adapt the new economic environment and the manufacturing. By analyzing the shortcomings of the traditional performance evaluation system under the new competitive environment, this paper build system of comprehensive performance evaluation on the base of the activity-based costing method been introduced by the paper. In this way, the traditional performance evaluation system, which works mainly on the financial indicators, is expanded into a more perfect and effective comprehensive evaluation system. The aim of this paper is to introduce a relatively perfect performance evaluation tools for the enterprise, and help the enterprise to improve the level of management, to elevate outstanding achievement and to strengthen the enterprise’s core competitiveness.

Key words:Activity-based costing ; Cost Management; The performance evaluation

目 录

摘 要 1

关键词 1

一、绪论 2

(一)研究背景和意义 2

(二)国内外研究现状 2

1 国外研究现状 2

2 国内研究现状 3

(三)国内外研究现状评论 4

二、传统的企业业绩评价体系在新竞争环境下的缺陷 5

(一)单一的财务指标进行评价和考核不能全面反映真实的业绩 5

(二)只是对过往业绩的总结,缺乏对将来的指导 5

(三)长期稳定的考核标准不能够反映现实的真实业绩 5

(四)容易造成管理人员对财务数据的不当追求与操控 5

三、基于ABC构建业绩评价体系的总体思路 6

(一)作业成本法的基本理论 6

(二)基于ABC构建业绩评价体系的构成要素 6

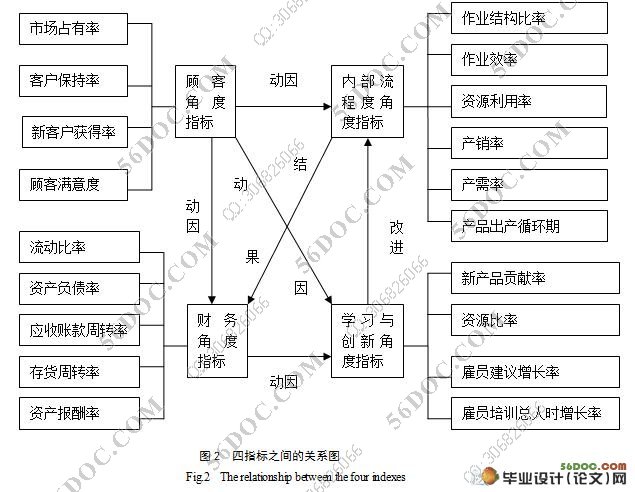

(三)基于ABC构建业绩评价体系各要素间的相互关系 7

四、基于ABC的业绩评价指标体系 7

(一)设置指标的原则 7

(二)基于ABC业绩评价指标的选择与计量 8

1 客户角度指标 8

2 内部经营方面指标 9

3 财务角度指标 11

4 学习与创新能力指标 12

五、基于ABC的业绩评价体系应用的优点和应该注意的问题 13

(一)基于ABC业绩评价体系应用的优点 13

1 管理者能有效地控制和调节成本的实施 13

2 财务指标与非财务指标相结合进行评价和考核能全面反映业绩 14

3 更好地管理企业内部经营 14

(二)应该注意的问题 14

1 把作业成本法与平衡计分卡相结合来完善业绩评价体系 14

2 要从各个角度分析作业及作业业绩 14

六、结束语 15

参考文献 15

致 谢 16